年度

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 1.

- 題型:問答題

- 難易度:尚未記錄

- 2.

- 題型:問答題

- 難易度:尚未記錄

- 3.

- 題型:問答題

- 難易度:尚未記錄

- 4.

- 題型:問答題

- 難易度:尚未記錄

- 5.

- 題型:問答題

- 難易度:尚未記錄

- 6.

- 題型:問答題

- 難易度:尚未記錄

- 7.

- 題型:問答題

- 難易度:尚未記錄

- 8.

- 題型:問答題

- 難易度:尚未記錄

- 9.

- 題型:問答題

- 難易度:尚未記錄

- 10.

- 題型:問答題

- 難易度:尚未記錄

- 11.

- 題型:問答題

- 難易度:尚未記錄

- 12.

Let {−0.8, −0.4, −0.2, 0.6} be a sample from a uniform distribution on [−1, 1]. Based on

this sample, please generate (simulate) a sample which is from an exponential

distribution 0.5e−x / 2 .(10%)

- 題型:問答題

- 難易度:尚未記錄

- 13.

- 題型:問答題

- 難易度:尚未記錄

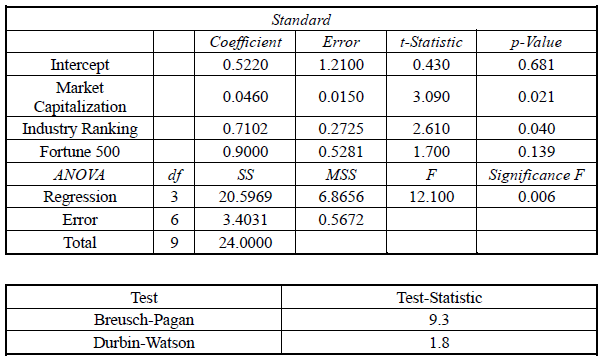

Multiple regression was used to explain stock returns using the following variables:

Dependent variable:

RET = annual stock returns (%)

Independent variables:

MKT = Market capitalization = Market capitalization / $1.0 million

IND = Industry quartile ranking (IND = 4 is the highest ranking)

FORT = Fortune 500 firm, where {FORT = 1 if the stock is that of a Fortune 500

firm, FORT = 0 if not a Fortune 500 stock}

The regression results are presented in the tables below

- 14.

The expected amount of the stock return attributable to it being a Fortune 500 stock

is closest to:- (A)

0.522.

- (B)

0.046

- (C)

0.710

- (D)

0.900

- 題型:單選題

- 難易度:尚未記錄

- 登入看解答

Multiple regression was used to explain stock returns using the following variables:

Dependent variable:

RET = annual stock returns (%)

Independent variables:

MKT = Market capitalization = Market capitalization / $1.0 million

IND = Industry quartile ranking (IND = 4 is the highest ranking)

FORT = Fortune 500 firm, where {FORT = 1 if the stock is that of a Fortune 500

firm, FORT = 0 if not a Fortune 500 stock}

The regression results are presented in the tables below

- 15.

The expected return on the stock of a firm that is not in the Fortune 500, has a

market capitalization of $5 million, and is in an industry with a rank of 3 is closest to:- (A)

2.88%.

- (B)

3.98%.

- (C)

1.42%.

- (D)

2.10%

- 題型:單選題

- 難易度:尚未記錄

- 登入看解答

Multiple regression was used to explain stock returns using the following variables:

Dependent variable:

RET = annual stock returns (%)

Independent variables:

MKT = Market capitalization = Market capitalization / $1.0 million

IND = Industry quartile ranking (IND = 4 is the highest ranking)

FORT = Fortune 500 firm, where {FORT = 1 if the stock is that of a Fortune 500

firm, FORT = 0 if not a Fortune 500 stock}

The regression results are presented in the tables below

- 16.

Does being a Fortune 500 stock contribute significantly to stock returns?

- (A)

Yes, at a 10% level of significance.

- (B)

Yes, at a 5% level of significance.

- (C)

No, not at a reasonable level of significance.

- (D)

No, not at a 15% level of significance.

- 題型:單選題

- 難易度:尚未記錄

- 登入看解答

Multiple regression was used to explain stock returns using the following variables:

Dependent variable:

RET = annual stock returns (%)

Independent variables:

MKT = Market capitalization = Market capitalization / $1.0 million

IND = Industry quartile ranking (IND = 4 is the highest ranking)

FORT = Fortune 500 firm, where {FORT = 1 if the stock is that of a Fortune 500

firm, FORT = 0 if not a Fortune 500 stock}

The regression results are presented in the tables below

- 17.

The p-value of the Breusch-Pagan test is 0.0005. The lower and upper limits for the

Durbin-Watson test are 0.40 and 1.90, respectively. Based on this data and the

information in the tables, there is evidence of:- (A)

only multicollinearity.

- (B)

only serial correlation.

- (C)

serial correlation and heteroskedasticity.

- (D)

only heteroskedasticity.

- 題型:單選題

- 難易度:尚未記錄

- 登入看解答

Multiple regression was used to explain stock returns using the following variables:

Dependent variable:

RET = annual stock returns (%)

Independent variables:

MKT = Market capitalization = Market capitalization / $1.0 million

IND = Industry quartile ranking (IND = 4 is the highest ranking)

FORT = Fortune 500 firm, where {FORT = 1 if the stock is that of a Fortune 500

firm, FORT = 0 if not a Fortune 500 stock}

The regression results are presented in the tables below

- 18.

Ron Working incorrectly uses the standard error of estimate instead of the standard

error of the forecast in his calculation of the confidence interval for the predicted

value from a simple linear regression with 26 observations. All else equal, the

confidence interval he calculates will be: (10%)- (A)

the same as the correct confidence interval.

- (B)

wider than the correct confidence interval.

- (C)

narrower than the correct confidence interval.

- (D)

wider than the correct confidence interval only if the R2 is greater than 0.50.

- 題型:單選題

- 難易度:尚未記錄

- 登入看解答