年度

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 100

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 99

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 98

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 97

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

- 96

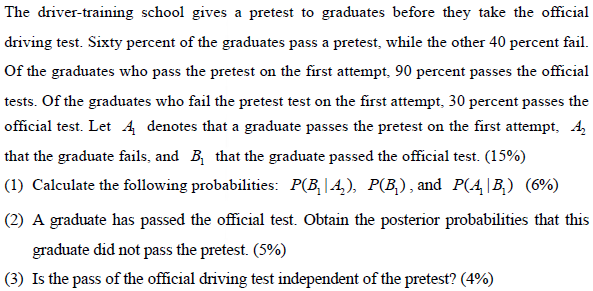

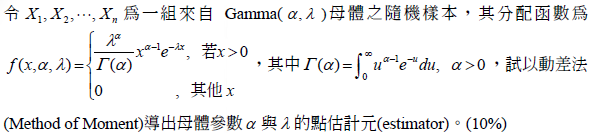

- 1.

- 題型:問答題

- 難易度:尚未記錄

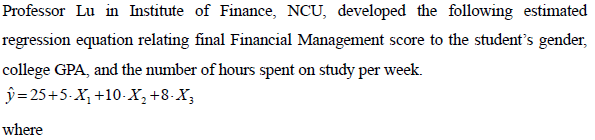

- 2.

A Finance Professor of National Central University reported that the mean of

book-to-market (BM) for firms listed in New York Stock Exchange (NYSE) is 0.82,

while the mean of OTC stocks is 0.77. The sample consists of 300 NYSE stocks and

400 OTC stocks. Based on historical data, the population standard deviations for the

BM can be assumed known at 0.30 for NYSE and 0.20 for OTC. (15%)

(1) Do the sample data indicate that NYSE stocks have a higher BM than OTC stocks?

Use α = 0.05 (6%)

(2) What is the p-value? (4%)

(3) What is the probability of committing a Type II error when the actual mean

difference of BM between NYSE and OTC stocks is 0.0629?

- 題型:問答題

- 難易度:尚未記錄

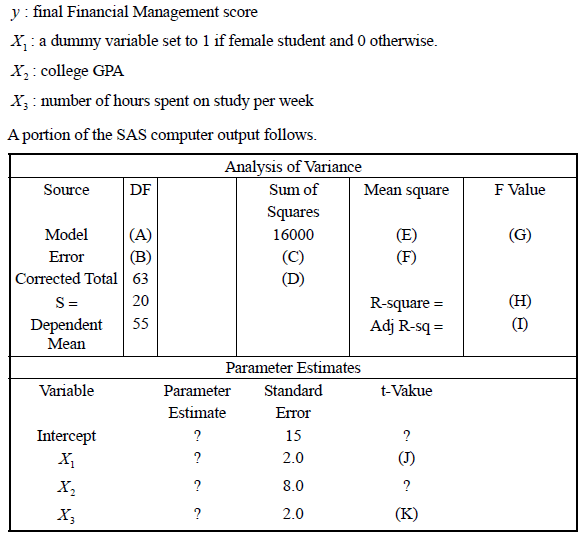

- 3.

(1) What are the vales of (A), (B), (C), (D), (E), (F), and (G)? (7%)

(2) What are the vales of (H), (I), (J), and (K)? (8%)

(3) Did the estimated regression equation provide a good fit to the data? Explain. (3%)

(4) Is gender a significant factor in Financial Management score? (2%)

- 題型:問答題

- 難易度:尚未記錄

- 4.

- 題型:問答題

- 難易度:尚未記錄

- 5.

- 題型:問答題

- 難易度:尚未記錄

- 6.

- 題型:問答題

- 難易度:尚未記錄

- 7.

- 題型:問答題

- 難易度:尚未記錄

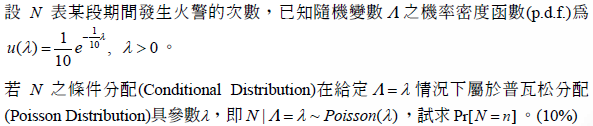

- 8.

令x為普瓦松分配(Poisson Distribution) Poission(λ )的隨機變數,請定義並計算此

分配之偏度(Skewness)與峰度(Kurtosis)。(10%)(提示:用動差生成函數(Moment

Generating Function))

- 題型:問答題

- 難易度:尚未記錄